Yesterday I was talking to a career coach who helped me through some blocks in my journey of disseminating financial knowledge to help people.

As it turns out, when it comes to finances the natural thought process goes to either struggling or prospering middle aged or retirees. They are the people who have the most issues with finances and do care about personal finance and wealth building the most. If one looks at the number of courses and videos targeted towards financial independence, how to retire with 401k or even sustain in retirement or simply building wealth, the largest audience is the middle aged person (probably in his/her forties).

However these are people who are also the know-it-all, seen-it-all kind. Even if they are not financially savvy, very few like to admit that and instead want to brag about the great house they have, the perfect stock that became a multi-bagger and so on. So for a techie like me to break into this financial web of self-denial and self-deceit in the very people I want to help, seems to me the biggest challenge.

As we (me and this awesome coach) discussed about this aspect in people, we realized that it is the younger version of themselves that would have done so much better, had they had exposure to right financial systems and knowledge.

I had been reading and practicing personal finance since 2005, yet when I moved to America in 2017, I learnt a whole new world of personal finance. And today I am amazed how far I came with my finances in just 3 years, one of which saw the worst pandemic in my lifetime. I wish I had this maturity when I started off in 2005 or even earlier when I started working in 1997.

As this ‘why’ becomes clearer in my mind and excites me, I could find a niche in the young adult population where they will be so much better starting off in the right financial foot.

Why is this younger generation better suited to start on finances? Well, millennial finance is nothing new and I may be adding another drop in the ocean but at that starting age, every drop of right advice helps. This is more so as the financial industry is full of mines (commission hungry salesman, the lure of credit cards, one dime down car purchase schemes) – a lot of the financial marketing machinery targeted towards the uninformed and the YOLO (You Only Live Once) generation.

Here are some questions that may be asked by a young graduate/professional as he/she tries to understand why all of this is important.

- The Why part has already been addressed in the above paragraphs. See below for more data on the problem or so called financial pandemic.

- Who to listen to? There are 5 potential teachers/mentors who can impart this education.

- School – It has been only lately that high schools have started teaching this subject. However it is a formal coursework, and not really suited to individual aspirations and potential.

- Parents – With due respect, most often parents end up giving biased advice or colored with their own dreams and fears. While this can be helpful, it can also be severely limiting due to the belief system of the family.

- Finance professionals – Professionals with financial degrees are often experts in the advanced parts of finance like portfolio analysis, investment recommendation etc. From that angle, the basics of personal finance are often ignored or these professionals assume the client is disciplined with his/her finances.

- Finance Gurus on Youtube and other medium – Well one has to know who is doing a service vs. just selling their courses. Almost 90% are just selling books and courses, including the very famous ones. As soon as the sale is done, the young client is on his/her own interpreting and applying the teachings.

- Non finance professionals – These are people who have learnt personal finance the hard way. However most non-finance professionals dismiss Personal Finance as a topic for the trained, or they act too smart chasing returns for their own portfolio. Technology professionals are good in analytical and modeling skills and by the time they reach the pinnacle of their career, even they have made a fair amount of financial mistakes which they cannot explain by math. This is because there is also a behavioral aspect of finance. Thus a combined knowledge from a non-finance perspective will help start the younger generation the right way.

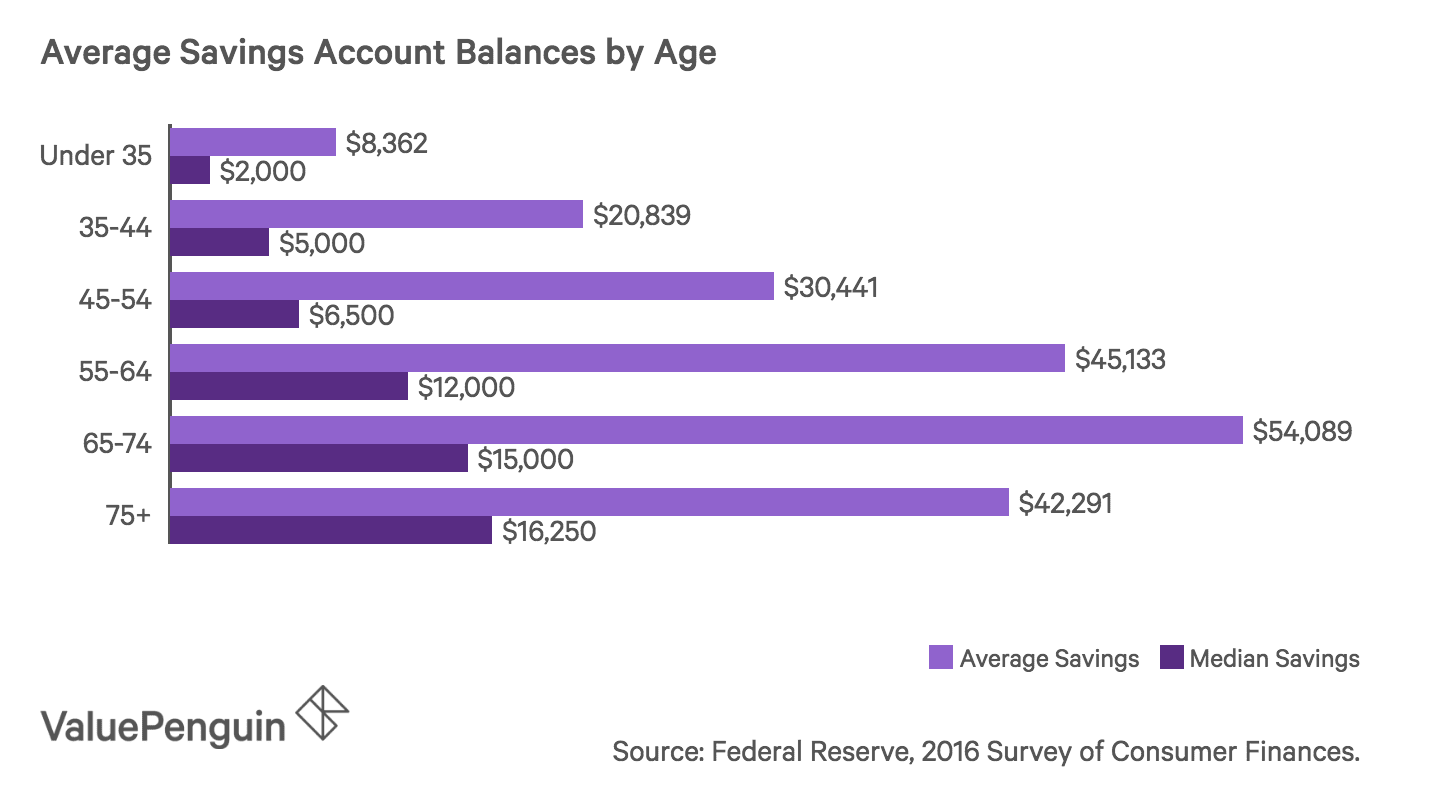

Having said the “why” and “who“, below are some basic statistics of why this Financial Literacy for Young Adults is increasingly so important in America and elsewhere in the world.

https://www.cnbc.com/2020/05/05/consumer-debt-hits-new-record-of-14point3-trillion.html

The below link talks about immigrant qualities regarding finance and entrepreneurship. Being an immigrant myself, I know why these aspects come naturally when one is born in a developing world. This has become a cliche and does not mean only immigrants have this quality, it is the right mindset and the foundations that are important, no matter which part of the world one belongs to.

https://www.cnbc.com/2019/06/19/two-great-financial-habits-we-can-learn-from-immigrants.html

Nowadays the consumer debt culture has caught up in India too, and the young adults are facing the same challenges as their counterparts in America.